|

Getting your Trinity Audio player ready...

|

Key facts:

- On September 28, 2025, Switzerland will decide on the abolition of the imputed rental value.

- Owners will benefit or lose from the abolition of the imputed rental value depending on their individual financial situation.

- The reform is regarded as one of the biggest tax policy decisions of recent decades.

The Swiss electorate said yes on September 28, 2025: the imputed rental value will be abolished and replaced by property taxes on second homes. This means that taxation of the notional rental value will no longer apply in future. At the same time, debt interest and maintenance deductions will no longer be possible. Depending on the financing and housing situation, this means either a noticeable reduction or additional costs for owners. Municipalities with many second homes will also have to reckon with falling tax revenues.

On September 28, 2025, the Swiss electorate will decide on one of the biggest tax reforms of recent decades: the abolition of the imputed rental value. The imputed rental value – i.e. the notional income that owners have to pay tax on on owner-occupied properties – has been criticized for years. The vote could herald a change in the system that will affect millions of owners.

What is the imputed rental value and why is it up for debate?

The imputed rental value was introduced in the 1930s to ensure equal tax treatment between tenants and owners. Since then, owners who live in their own home have been taxed on a notional rental value. At the same time, debt interest and maintenance costs can be deducted.

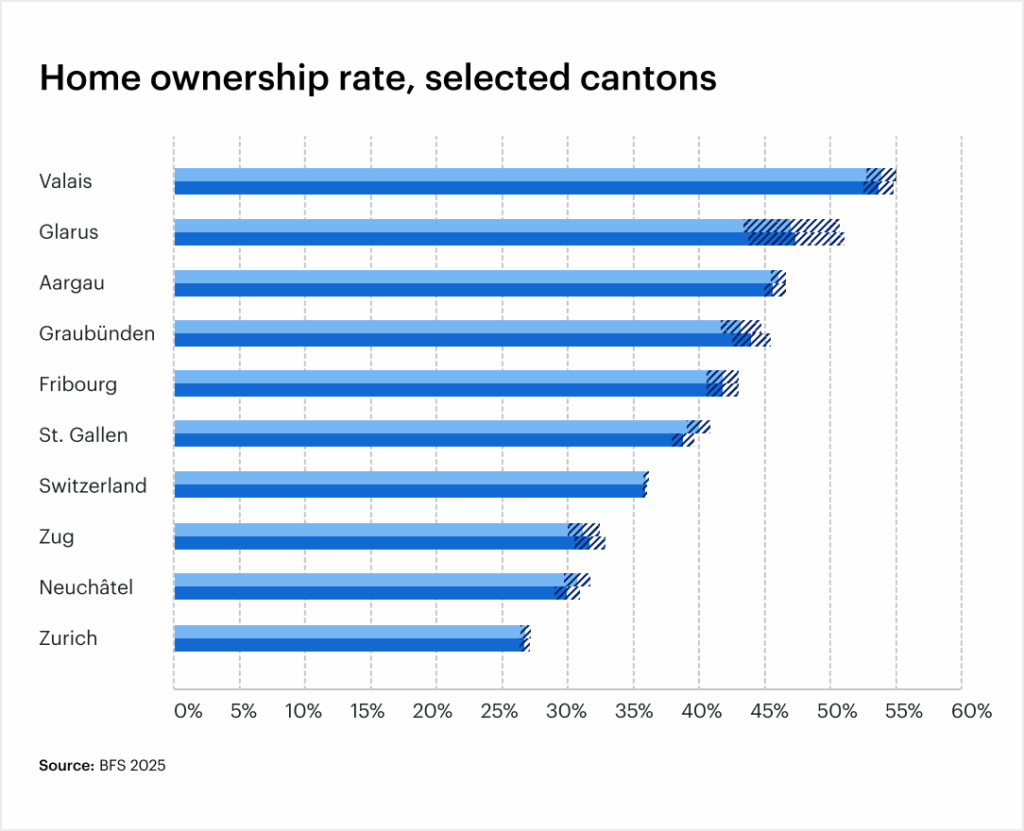

This system is highly controversial today. Critics see it as unilaterally favoring households with high mortgages. Proponents, on the other hand, emphasize that this is the only way to ensure a balance between renting and owning. With a home ownership rate of 36%, the number of people affected is a third of the Swiss population.

The planned reform of the imputed rental value

On September 28, the Swiss people will vote on the introduction of a property tax. If this is accepted, it would entail the abolition of the imputed rental value for primary and secondary residences. At the same time, debt interest deductions and deductions for maintenance and renovations would be abolished. A reduction applies for the transitional period: in the first year, couples can still claim up to CHF 10,000 and single people up to CHF 5,000 in debt interest, but this amount will fall to zero over ten years.

This fundamentally changes the tax logic for owners: they no longer have to pay tax on notional income, but can no longer deduct their financing and maintenance costs.

Owner-occupied rental value reform: implications for owners

The effects of the reform of residential property taxation depend heavily on the individual situation.

- Debt-free owners: Those who have largely amortized their mortgage are among the winners. The imputed rental value no longer applies without any relevant deductions being made. For many older households, this means a noticeable tax reduction.

- Heavily indebted households: Owners with large mortgages lose the opportunity to deduct debt interest. This significantly increases the annual net costs.

- Properties in need of renovation: maintenance costs and energy-related investments are no longer tax-deductible. The reform will have a particularly negative impact on owners planning modernization or energy-efficient renovations.

- Impact on climate policy: Building and energy associations warn that renovations could decline, making it more difficult to achieve climate targets.

This shows that the reform is clearly advantageous for debt-free households, while heavily indebted owners or renovators must expect additional burdens.

Second homes and municipalities

There is a special focus on second homes in tourist regions. They are traditionally valued at high imputed rental values, which often leads to a noticeable tax burden for owners. The abolition will reduce this burden. At the same time, however, all deductions are eliminated, which worsens the bill for heavily financed properties or houses with high maintenance requirements.

The municipalities are feeling the change even more keenly. In regions such as Graubünden, Valais and Ticino, a significant proportion of tax revenue comes from the imputed rental value of second homes. If this source of income disappears, many municipalities will be faced with significant losses. In order to finance infrastructure and services, they would either have to increase their tax rates or tap into other sources of funding. The reform will therefore not only have an impact on owners, but also on municipal budgets and ultimately the attractiveness of the regions affected.

Abolition of imputed rental value: consequences for buyers and sellers

The reform also affects the real estate market as a whole. Buyers with high debt financing lose the opportunity to deduct debt interest from tax. This makes purchases with high financing requirements less attractive. Buyers with a high level of equity, on the other hand, will benefit as they will hardly lose any deductions and will profit from the tax relief resulting from the abolition of the imputed rental value.

For sellers, this means that the calculations of potential buyers will change. Demand could shift: Properties with low maintenance costs and good energy efficiency will remain attractive, while properties in need of major renovation could lose value. Anyone planning a sale should factor these developments into their strategy and check whether an earlier sale would pay off better.

Sample calculation for the abolition of imputed rental value

Assumptions (simplified figures, for illustration purposes):

Rental value: CHF 15,000 per year (approx. 60% of the market rent of a typical property). Debt interest: CHF 20,000 per year. Maintenance/renovation costs: CHF 5,000 per year. Average marginal tax rate: 30%.

1. owner without mortgage (debt-free)

Today:

- Taxable imputed rental value: CHF 15,000

- No deductions

- Tax burden: CHF 15,000 × 30% = CHF 4,500

After the reform:

- No imputed rental value

- No deductions necessary

- Tax burden: CHF 0

Result: Savings of CHF 4,500 per year

2. owner with high mortgage and maintenance (second home)

Today:

- Taxable imputed rental value: CHF 15,000

- Deductions: CHF 20,000 debt interest + CHF 5,000 maintenance = CHF 25,000

- Net income for tax purposes: -CHF 10,000 (i.e. deductions exceed imputed rental value)

- Tax burden: CHF 0, possibly even tax reduction through other income

After the reform:

- No imputed rental value

- No more deductions possible

- Tax burden: CHF 0

Result: effective additional burden of CHF 3,000 to CHF 7,500 per year, as the deductions no longer apply and can no longer be offset against other income.

Voices from politics and business

The debate is being conducted with great intensity. Proponents see the reform as a simplification of the tax system and long overdue relief for many owners. Homeowners’ associations argue that the current practice is illogical and sets the wrong incentives, as it encourages debt.

Opponents, on the other hand, emphasize the risks. Building and energy associations warn that the loss of tax incentives could reduce the renovation rate. Municipalities in tourist regions are expecting tax losses in the double-digit millions, which would be difficult to compensate for. Critics also point to the fiscal aspect: the federal government and cantons estimate total losses of around CHF 1.7 billion per year, depending on interest rates.

Conclusion: Abolition of imputed rental value has far-reaching consequences

The abolition of the imputed rental value represents a fundamental change to the system. For debt-free owners, it means noticeable relief, while households with high mortgages or major renovation needs will be more heavily burdened in future. Buying and selling decisions will also change: buyers with strong capital will benefit, while debt-financed households will calculate more cautiously. The vote on September 28, 2025 will therefore not only decide on a tax model, but also on the future dynamics of the Swiss real estate market.

FAQ

1. what impact will the reform have on mortgage strategy?

With the abolition of debt interest deductions, high debt financing will become less attractive from a tax perspective. Owners are likely to be more inclined towards amortization in order to reduce their burden. Banks are expecting a shift towards lower mortgage ratios.

2. will energy-efficient renovations still be subsidized in the future?

At federal level, the option to deduct investments from tax is no longer available. However, subsidy programs remain in place at cantonal and communal level. Owners must rely more on direct subsidies instead of tax deductions.

3. what consequences does the reform have for municipalities with many second homes?

In tourist regions, municipalities fear considerable tax losses, as the imputed rental value of second homes is an important source of income. Financing public infrastructure could become more difficult, which could lead to higher tax rates in the long term.

4. should owners with a planned sale wait for the vote?

This depends on the buyer structure. Buyers with a high level of debt financing will lose tax advantages as a result of the reform, which may dampen their demand. Buyers with strong capital, on the other hand, will benefit. Anyone planning a sale should check whether a deal before the vote will attract more potential buyers.

Data are without guarantee. The information on these Internet pages has been carefully researched. Nevertheless, no liability can be assumed for the accuracy of the information provided.