Since January 1, 2025, new regulatory changes have come into force in Switzerland as part of Basel III, which require banks to hold more capital. The aim of the new Capital Adequacy Ordinance is to strengthen the stability of the banking system by requiring financial institutions to deposit more equity for loans granted. The consequence for property buyers, owners and investors: stricter lending criteria, rising mortgage interest rates and less flexibility in financing.

But what does this mean in concrete terms for property owners and buyers?

What impact will Basel III have?

Basel III is an international regulatory framework for banks that was developed by the Basel Bank for International Settlements (BIS) after the 2008 financial crisis. It tightens capital and liquidity requirements in order to increase the stability of the banking system and reduce systemic risks.

Key points of the reform:

- Stricter capital requirements: Banks must deposit more equity for mortgage loans, especially for high-risk financing such as commercial real estate or highly leveraged buyers.

- Higher risk weights for real estate loans: Loans with high loan-to-value ratios are given higher risk weights, making lending more restrictive.

- Stricter liquidity requirements – The new regulations, such as the Net Stable Funding Ratio (NSFR) and the Liquidity Coverage Ratio (LCR), require banks to have more stable refinancing and higher short-term liquidity reserves, which can make real estate financing more expensive.

- Limitation of debt financing – Stricter lending criteria can lead to higher equity requirements for buyers and investors, making large-volume projects in particular more difficult.

- Increased transparency requirements – banks must carry out more detailed risk assessments for real estate financing, especially for non-standardized or complex financing models.

The impact will not only affect future home buyers, but also existing owners who are planning to extend or adjust their mortgage.

Stricter lending standards: Who still gets a mortgage?

The regulations mean that banks are now acting more strictly when granting mortgages. For borrowers, this means

- Higher capital requirements: Anyone who previously obtained a mortgage with 20% equity could have to meet stricter capital requirements, depending on the bank’s risk assessment. Increased capital requirements already apply in Switzerland, particularly for mortgages above 66.67% (two-thirds limit).

- Stricter credit checks: Banks are looking even more closely at applicants’ income, reserves and level of debt.

- Higher interest rates for higher-risk borrowers: Anyone with a weaker credit rating or a high level of debt financing must expect higher interest rates or additional collateral.

- More restrictions for the self-employed: Anyone with an irregular income must be prepared for stricter obligations to provide evidence.

Longer review processes – banks have to carry out more extensive risk analyses, which can delay loan approval.

Rising mortgage rates: is a fixed-rate mortgage worthwhile now?

Is a fixed-rate mortgage worthwhile now? Whether a fixed-rate mortgage is worthwhile now depends on the development of interest rates, your own financial situation and your willingness to take risks. Basel III regulations can indirectly increase refinancing costs for banks, especially for riskier mortgages. However, the most important factor for mortgage interest rates remains the interest rate environment, which is determined by the Swiss National Bank (SNB) .

How will the new rules affect existing mortgages?

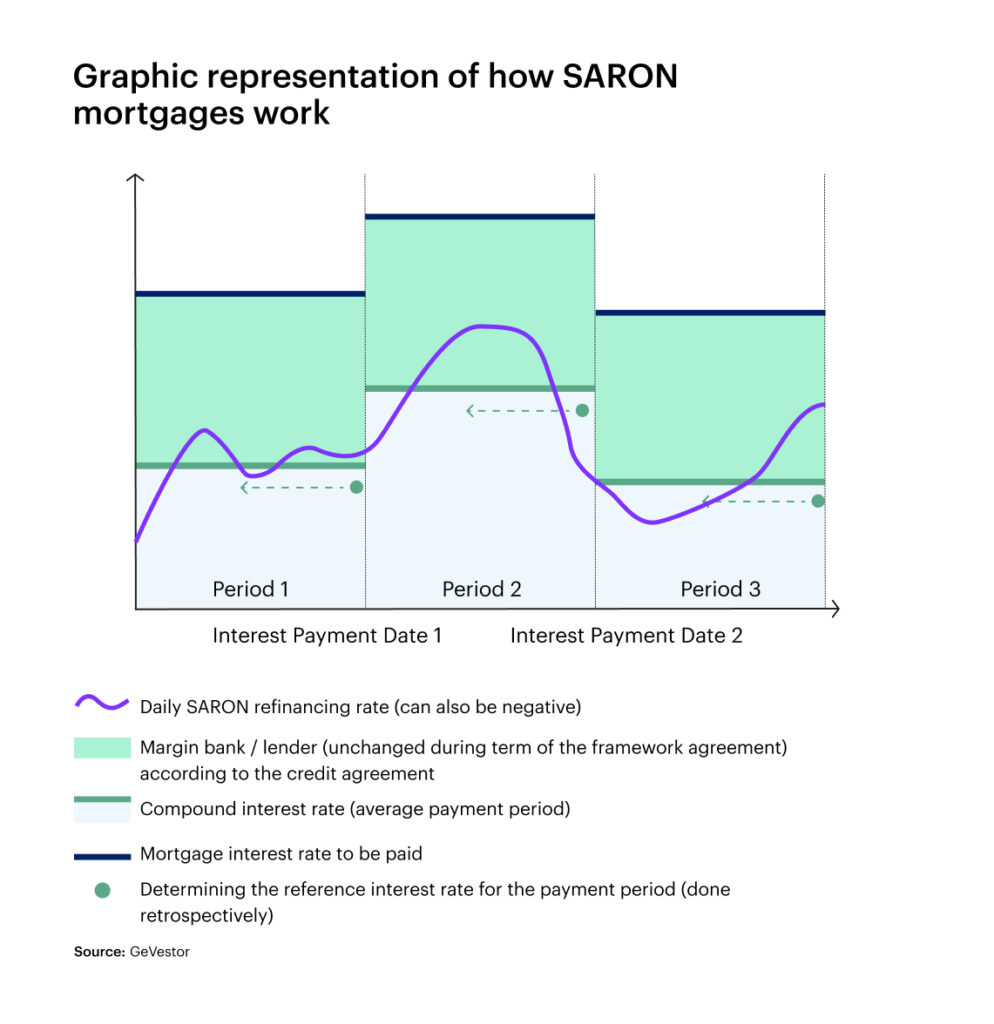

Existing mortgages, particularly SARON mortgages, may be affected by rising bank refinancing costs. However, as SARON interest rates are market-linked, the development depends primarily on the SNB’s monetary policy.

Which financing strategies make sense now?

The new Basel III rules require a well-thought-out strategy for property buyers and owners. One way of counteracting rising financing costs is to have a higher equity ratio. Those who can finance more than 20% of the purchase price themselves generally benefit from better interest conditions. It is equally important to optimize your own credit rating – this means reducing debt and demonstrating a stable income.

For many borrowers, it can also make sense to split their mortgage into several tranches with different terms in order to benefit from more flexible conditions. While a long-term fixed-rate mortgage offers security, shorter terms or a SARON portion can provide additional flexibility.

Conclusion: What should property owners and buyers do now?

Basel III brings stricter hurdles for mortgages, but financial disadvantages can be minimized with the right preparation. Early financial planning, comparing loan conditions and optimizing your own credit rating are essential. Mortgage holders should also consider whether a fixed-rate mortgage with a long-term fixed interest rate or a more flexible form of financing is the better choice.

If you inform yourself now and act in good time, you can secure solid real estate financing despite the new regulations.

Data are without guarantee. The information on these Internet pages has been carefully researched. Nevertheless, no liability can be assumed for the accuracy of the information provided.