|

Getting your Trinity Audio player ready...

|

Key facts:

- Installment plan enables home ownership even without 20% equity.

- Constant rental installments instead of interest rate risk, because monthly payments can be planned for years to come.

- Tighter credit requirements and high prices make installment plan an attractive solution in 2025.

Access to home ownership remains restricted for many households in Switzerland – in particular due to high real estate prices, stricter financing requirements and an increasingly scarce supply. In this environment, a previously neglected form of financing is coming back into focus: the installment plan. This model will become much more relevant in 2025 and opens up realistic prospects for buyers who have a stable income but not enough equity to obtain a conventional mortgage.

What is Rent-To-Own?

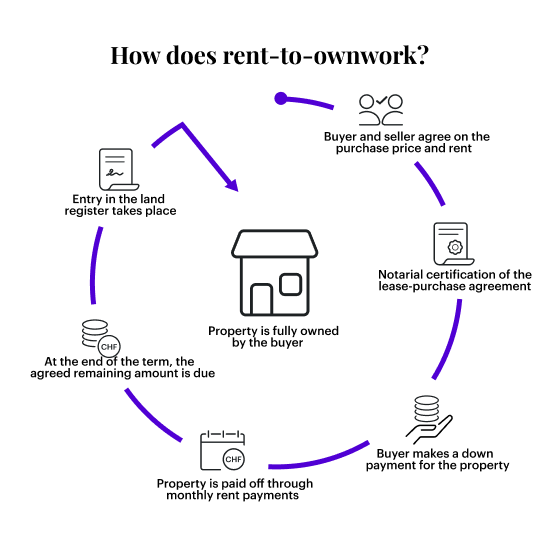

Installment plan is a hybrid form between renting and purchasing property. A rental agreement is concluded which also stipulates an option or obligation to purchase at a later date. During the term of the contract, the buyer already lives in the property and pays a monthly rent, part of which is offset against the future purchase price as a down payment. The actual transfer of ownership only takes place at the end of this term – usually after several years.

This model is common in Switzerland as it offers interesting opportunities, particularly for buyers with a solid financial starting position but a lack of start-up capital. Rent-to-own creates planning security, allows you to move into your desired property early and enables you to build up equity over the years.

Why will installment plan become more important in 2025?

Basel III tightening

Since January 2025, stricter capital requirements have applied in Switzerland in accordance with the Basel III regulations. As a result, banks will act much more cautiously when granting mortgages and place higher demands on borrowers. Younger buyers and working people with regular but low savings are particularly affected – they often no longer meet the minimum criteria required for financing. Installment plan avoids this entry hurdle as it works without a traditional down payment.

Persistently high real estate prices

The Swiss real estate market will continue to be characterized by price increases in 2025. According to current market analyses, average prices are around CHF 7,572 per square meter for single-family homes and CHF 8,859 for condominiums – and the trend is rising. Especially in cities and conurbations, these price levels are hardly affordable for many prospective buyers. A lease-purchase offers the opportunity to secure the desired location at an early stage.

Lower mortgage interest rates, but not accessible to all

The Swiss National Bank lowered its key interest rates in the course of 2024, resulting in noticeably lower mortgage rates. However, not everyone can benefit from this: Those with less than 20 percent equity or who are only just above the affordability limits are often not considered by banks. Here, installment plan offers an alternative bridge to ownership without having to provide full financing immediately.

Advantages of installment plan at a glance

A key advantage of installment plan is the lower entry threshold. The property can be purchased without a large initial investment and built up financially over the years. In addition, the purchase price is contractually fixed: The future price is already defined when the contract is signed, regardless of how the market develops. This creates security for buyers and protects against price increases.

The property is available for use right from the start of the contract. This means that living in your own home does not just begin with the entry of ownership, but immediately. During the term of the contract, equity is continuously saved through the rental payments – an amount that is offset directly against the later purchase. There is also flexibility when it comes to the final financing: The outstanding purchase price can be covered by savings or a traditional mortgage.

Challenges and risks

Despite the advantages, installment plan also entails risks. For example, the monthly installments are usually higher than the usual rental level, as they include a kind of purchase advance in addition to the usage fee. It is also a longer-term contractual commitment: Anyone who wants to get out of the contract prematurely risks financial losses – for example, due to the forfeiture of partial payments already made.

Another critical point is the final financing. At the end of the contract term, the outstanding purchase price must be paid – which may require a new credit check or financing. If there is a negative development in the real estate market, the originally agreed purchase price may even be higher than the current market value.

Who is installment plan suitable for?

Installment plan is particularly suitable for buyers who have long-term housing prospects but do not yet have the necessary funds or requirements for a conventional mortgage. This includes, for example, self-employed people with seasonally fluctuating income, households with low equity or couples who are currently still renting but would like to buy their own home in the medium term. People who have already found their dream property but are still in the preparation phase for later financing will also benefit.

Conclusion

Installment plan will be far more than a niche product in 2025. The model offers realistic prospects for households that do not yet have a mortgage but still want to move into property ownership. Especially in a market environment characterized by high prices, regulatory requirements and uncertain financing conditions, installment plan creates new scope. It remains crucial to carefully examine the terms of the contract – particularly with regard to purchase price commitment, residual debt and withdrawal options. If you are well informed, you can enter the real estate market strategically with an installment plan.

All data are without guarantee. The information on these Internet pages has been carefully researched. Nevertheless, no liability can be assumed for the accuracy of the information provided.